When the borrowers miss few EMI payments, one fear immediately starts troubling them:

- “Can the bank file a case against me?”

- “Can I go to jail for not paying the loan?”

- “Can the police come to my house?”

- “Will the bank seize all my property?”

A common source of anxiety for many people is receiving repeated harassing phone calls from collection agents or receiving legal notices or having someone threaten them with legal action through WhatsApp (or some other form of electronic communication). Many people wait until they’re already in a stressful situation before seeking help from an attorney. They may have just lost their job; their business may have failed; they may have had unexpected medical expenses that have drained their financial resources; or they may already have several debts that they’re working on repaying.

In situations like this, the aggressive communication style used by collection agencies can create even more anxiety. Many borrowers will think that because they defaulted on the loan, they might be going to prison (as a result of criminal charges). Under Indian Law, this is not the case.

Banks and financial institutions do have legal remedies to recover their money. However, every loan default does not become a criminal case. There is a major legal difference between genuine financial inability and intentional fraud.

Understanding this particular distinction can protect you from the unnecessary fear, wrongful harassment, as well as costly mistakes.

What Loan Default Actually Means

Loan defaults are defined as the event that occurs when a person fails to pay back a loan as required under the terms of the agreement for repayment of the loan.

A borrower may default on money borrowed through a personal loan, business loan, home loan, vehicle loan, education loan, credit card, or any other form of lending that has been secured against collateral.

You will not automatically be considered a legal defaulter because you have missed a single EMI but if you do not make payments over a period of time, recovery actions may be taken against you.

According to banking guidelines, any loan that has not had either the principal or interest paid for a period in excess of 90 days is to be classified as a Non-Performing Asset (NPA).

This is the stage where the bank may begin more serious recovery action. But even then, the nature of action depends entirely on the type of loan, security involved, and borrower conduct.

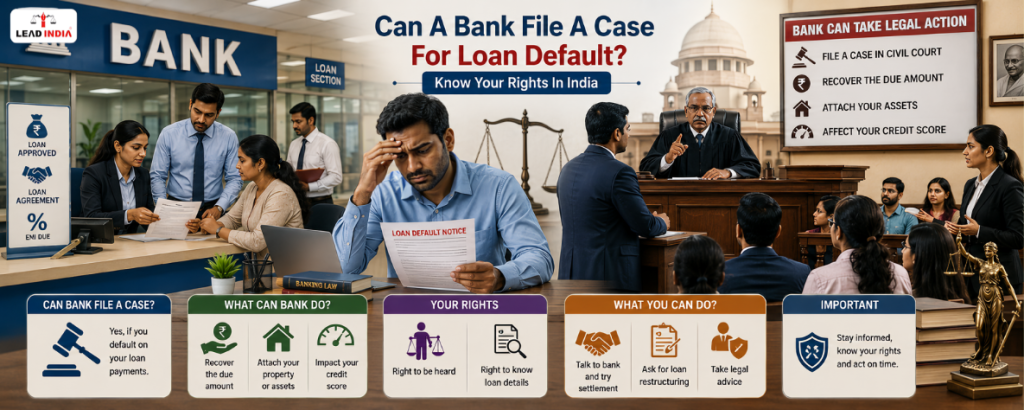

Can a Bank Actually File a Case for Loan Default?

The short legal answer is: Yes, the bank can file the case for loan default in India. But the more important question is: What kind of case? This is where most borrowers get confused.

Typically speaking, in the case of true loan defaults, the issue will be resolved as a civil dispute for recovery of the loan amount as opposed to a criminal prosecution.

If you took out a legal loan, signed all documents in good faith, and then later became unable to repay due to some legitimate financial hardship, then a lender can still pursue recovery of their funds from you; however, this action does not make you automatically liable for a criminal offence.

If you obtained the loan through fraudulent actions (e.g., forgery of documents or creating fictitious property documents or providing false income records) or through intentional acts to cheat someone or redirect loan funds, this could potentially lead to civil and/or criminal consequences.

So, the legal position is simple: Financial default is usually civil. The fraudulent conduct may then become criminal.

Can You Go to Jail for Not Paying a Loan?

This is probably the most searched question. The legal answer is:

A person’s failure to repay a loan as a result of being unable to afford it does not automatically mean that they will be jailed. This has been established in many cases in India by the courts.

The courts have repeatedly ruled that where a person cannot pay their debt due to reasons beyond their control (such as poor crops or loss of employment), the lack of discipline and the intention to repay does not constitute a criminal act on the part of the debtor.

However, jail-related exposure may arise if there is evidence that:

- The borrower submitted forged documents,

- Misrepresented assets,

- Created fake employment records,

- Obtained the loan with dishonest intention from the beginning, or

- Diverted secured funds fraudulently.

This distinction is extremely important. A borrower in financial distress is not automatically the criminal offender.

What Usually Happens After You Miss Loan Payments?

Most borrowers believe if they miss an EMI, police will be contacting them right away. This is not how it works, in a typical case:

- They will initially start by contacting the borrower with reminders through phone calls, text messages and e-mails; if the payments remain overdue after that, internal recovery agents will contact them.

- In secured loans, if the account becomes NPA, SARFAESI proceedings may be initiated in eligible cases.

- If the amount is substantial, recovery proceedings before appropriate legal forums may begin.

- The process is fully gradual and not instantaneous.

- This is why the borrowers should never ignore the notices.

- The early communication often creates the room for restructuring, settlement, or the negotiated resolution.

Legal Remedies Available to Banks

- Indian law gives banks multiple legal recovery options.

- The exact remedy depends on the nature of lending.

Civil Recovery Proceedings

- Most loan defaults are contractual disputes.

- If the borrower has failed to repay, the bank can approach civil forums for money recovery.

- The purpose here is not punishment.

- The objective is recovery of outstanding dues, interest, and legal costs.

- This is one of the most common legal routes.

Debt Recovery Tribunal (DRT)

- For qualifying debt recovery matters, banks may approach the Debt Recovery Tribunal.

- The DRT system exists to provide a faster recovery mechanism compared to ordinary civil courts.

- Banks may seek recovery certificates, enforcement orders, and asset-related recovery remedies.

- If you receive DRT summons, ignoring them can seriously weaken your position.

- Legal defence should be prepared immediately.

SARFAESI Proceedings

- This is one of the most feared legal mechanisms.

- Under the SARFAESI Act, secured creditors can enforce security interests in qualifying cases without first filing a traditional civil suit.

- This generally applies where secured assets are involved.

- The process usually begins with a statutory demand notice.

- Borrowers are given an opportunity to respond.

- If compliance does not happen, further enforcement measures may follow, including possession-related action concerning secured property.

- However, banks cannot randomly seize assets without following legal procedure. Improper SARFAESI action can be challenged.

Insolvency Proceedings

- In certain commercial or the corporate debt scenarios, the insolvency remedies may also become very much relevant.

- This usually depends on the nature of the borrower and statutory thresholds. Not every retail borrower falls into this category.

Can Police Arrest You for Loan Default?

- In ordinary loan default cases, police arrest is not the standard legal consequence.

- Police do not function as private recovery agents for banks.

- However, if the bank alleges for criminal fraud, cheating, forged documentation, or any deliberate deception, the criminal complaints may be pursued. That changes the legal situation.

- Therefore, the borrowers need to understand whether the issue is purely repayment-related or it is fraud-related.

- If the dispute is genuinely about repayment inability, police threats are often legally questionable.

Rights of Borrowers Against Harassment

- Many borrowers are unaware that Indian law protects them from unlawful recovery practices.

- A bank may recover dues lawfully. But harassment is not lawful recovery.

- The recovery agents cannot threaten you, abuse you, publicly humiliate you, or intimidate your family.

- They cannot behave like enforcement gangs.

- The Supreme Court in ICICI Bank v. Prakash Kaur strongly criticized unlawful coercive recovery practices.

- The Court made it clear that recovery must happen strictly through lawful means.

- Borrowers retain dignity and legal protection even during default.

Can Recovery Agents Visit Your Home?

Yes, lawful recovery communication may include visits in accordance with applicable norms. But a lawful visit does not mean harassment.

Recovery personnel cannot:

- Threaten violence,

- Abuse family members,

- Create neighbourhood humiliation,

- Publicly shame borrowers,

- Force signatures, or

- Use intimidation tactics.

If this happens, legal remedies may be available.

Can a Bank Freeze Your Salary Account?

- This is another area of widespread confusion.

- Banks cannot arbitrarily freeze unrelated accounts merely because a loan default exists, unless supported by lawful authority or contractual/legal basis.

- Different legal scenarios may then produce different outcomes, especially where the lending arrangements, set-off rights, court orders, or the regulatory mechanisms are involved.

- But arbitrary freezing without due process can be challenged. Each case depends on facts.

What If You Receive a Loan Recovery Notice?

The worst mistake borrowers make is ignoring legal notices. A legal notice does not mean the case is already lost. It means action has begun.

The first step is to carefully review:

- The outstanding claim,

- Interest calculations,

- Penal charges,

- Default period,

- Security details, and

- Legal basis invoked.

Errors are not uncommon. Sometimes inflated charges or procedural defects exist. A professional review can identify whether the notice is legally valid.

Can You Settle a Loan Legally?

Yes. Loan settlement is often a practical option. Many borrowers assume that once default begins, litigation becomes unavoidable.

That is not always true. Depending on the lender’s internal policy, restructuring, rescheduling, negotiated repayment, or the One-Time Settlement (OTS) may get explored.

However, the borrowers should understand the consequences before agreeing.

- Settlement may affect credit history.

- Poorly drafted settlements can create future disputes.

- Verbal promises from recovery staff should never be blindly trusted.

- Always insist on the written clarity.

What If You Genuinely Cannot Pay?

Indian law recognizes practical realities. Financial hardship occurs. Job loss, business collapse, medical emergencies, economic downturns, or family crises can severely affect the repayment capacity.

If at all the repayment has genuinely become impossible:

- Communicate early,

- Maintain written records,

- Avoid disappearing,

- Request restructuring, if possible,

- Seek legal review of notices, and

- Avoid panic decisions.

Silence usually worsens matters. Structured negotiation often creates better outcomes.

Important Supreme Court Judgments Borrowers Should Know

Indian courts have shaped borrower protection significantly.

The Supreme Court analysed the SARFAESI framework and determined that safeguards against arbitrary recovery action must be upheld in the case of Mardia Chemicals Ltd. v. Union of India. This case is of utmost significance in regards to secured loan disputes.

In the case of ICICI Bank v. Prakash Kaur, the court prohibited the use of aggressive recovery tactics by banks and advised that banks are not permitted to use intimidation or physical force to recover debts. For this reason, this decision is still widely referenced by borrowers suffering from recovery harassment.

In the case of Sardar Associates v. Punjab & Sind Bank, the court discussed fairness when dealing with settlement related issues.

Therefore, these decisions demonstrate that although banks have the right to recover legally, borrowers have enforceable protections as well.

Practical Mistakes Borrowers Must Avoid

- When the panic begins, the borrowers often make damaging decisions.

- One common mistake is ignoring notices entirely.

- Another is making verbal commitments without documentation.

- Some borrowers sign papers under pressure without understanding the consequences.

- Others trust informal settlement assurances from recovery agents.

- Some stop communicating completely, which often escalates legal exposure.

- The smarter approach is structured legal and financial response.

What To Do Immediately If You Are Facing Loan Default

- If at all your loan has become difficult to manage, the practical action matters.

- Understand whether the issue is temporary cash flow stress or long-term inability.

- Gather all documents including loan agreement, repayment history, notices, and communication records.

- Check whether the lender’s calculations are accurate or not.

- Avoid the emotional reactions to threatening calls.

- Obtain the proper legal advice before taking the irreversible decisions.

Legal Remedies Available to Borrowers

Borrowers are not at all powerless. Depending on the circumstances, the remedies may include:

- Challenging improper SARFAESI action,

- Approaching DRT where applicable,

- Filing complaints regarding harassment,

- Aaising banking grievances,

- Seeking compensation for unlawful conduct, or

- Pursuing appropriate legal proceedings.

- The right remedy depends on facts.

Final

So, can the bank file a case for the loan default?

Yes. But not every loan default is a criminal matter. Banks can legally recover dues through structured legal mechanisms. However, borrowers cannot be treated as criminals merely because of genuine financial hardship. The law balances the lender’s recovery rights with the borrower’s dignity and legal protection. Understanding that balance is very much important.

How Lead India Can Help

Legal help can greatly improve your situation if you have received a bank recovery notice; if you received a SARFAESI notice, DRT summons or have been threatened by a recovery agent; or if you cannot pay your EMI on time.

Lead India gives borrowers a clear understanding of their rights and can also help you carefully evaluate any notices you have received. You can dispute any unlawful recovery attempts against you, explore various options to settle out of court and receive other appropriate legal advice depending on your situation.

One can talk to lawyer from Lead India for any kind of legal support. In India, free legal advice online can be obtained at Lead India. Along with receiving free legal advice online, one can also ask questions to the experts online free through Lead India.

FAQs

1. Can the bank file FIR for the loan default?

Not for ordinary repayment inability alone. The criminal allegations generally require fraud, cheating, forged documents, or dishonest conduct.

2. Can I go to jail for the unpaid personal loan?

The mere inability to repay does not automatically lead to imprisonment.

3. Can recovery agents threaten me?

No. The harassment, intimidation, abuse, or the unlawful pressure may legally be challengeable.

4. Can the bank seize my house immediately?

No immediate arbitrary seizure is not the legal process. Due procedure applies.

5. Can I settle all of my defaulted loans?

Yes, depending on lender policy and case facts.

6. Can the police come to my home for the loan default?

Ordinary civil default does not automatically trigger police action.